For high-income executives, controlling when you pay taxes on your income matters as much as how much you earn. Deferred compensation plans, most commonly structured as nonqualified deferred compensation (NQDC) plans, allow executives to defer salary, bonus, or other compensation into a future year rather than recognizing it today, when your income and tax rate are typically at their peak.

The core logic is simple: earn in your highest-bracket years, get paid in your lower-bracket years. For an executive earning $750,000, deferring $100,000 today could mean the difference between paying 37% federal tax now versus 22–24% in retirement – a difference that compounds meaningfully over time.

Tax Bracket Management

Where executive deferred compensation becomes especially powerful is in managing your effective tax rate across multiple years. Because distributions are taxed as ordinary income when paid, the goal is to “fill up” lower brackets gradually rather than trigger large income spikes in any single year.

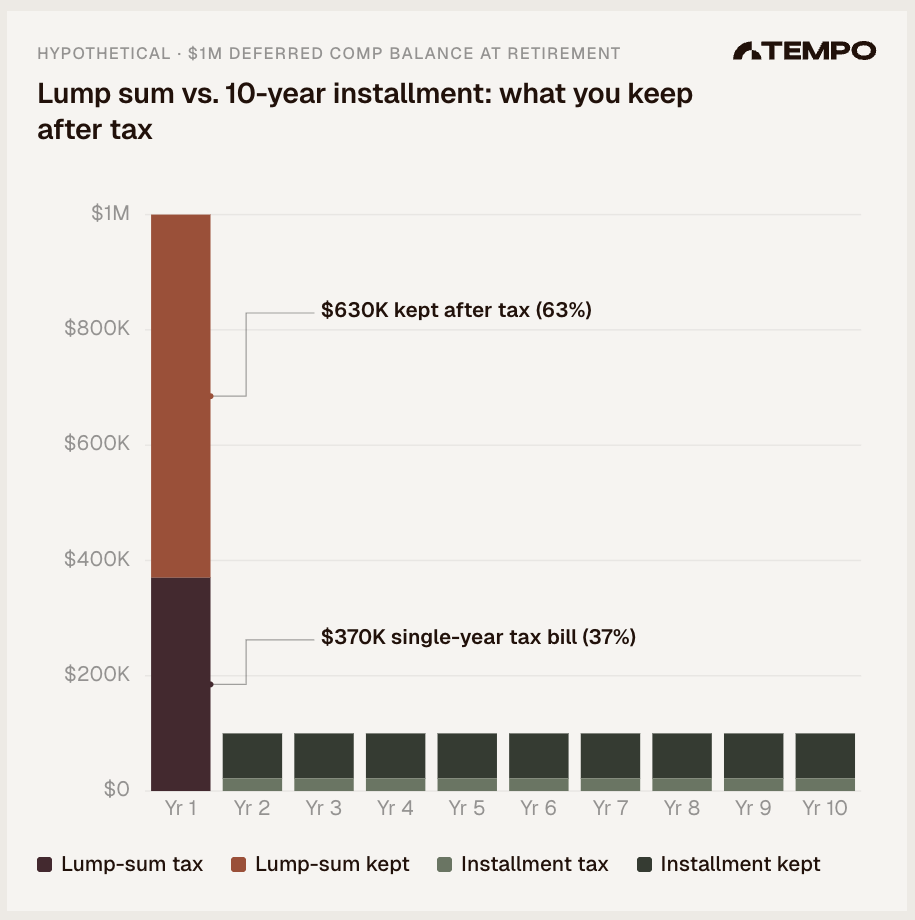

The chart below illustrates the difference between two approaches for an executive with $1 million in deferred comp: taking a lump sum in year one of retirement versus spreading distributions over 10 years at $100,000 per year.

In this hypothetical, total tax paid on the lump sum is $370,000. If taken instead as 10 payments of $100,000 spread over 10 tax years, the tax rate drops to 22%, or $220,000 total. That's a tax savings of $150,000.

Note: these figures are illustrative estimates only and do not constitute a recommendation or tax advice. Every executive’s situation – including filing status, other income sources, state of residence, and plan terms – is unique. Effective planning of this nature requires a coordinated advisory team: a wealth manager to model the income strategy and a CPA to optimize the tax outcome. The interaction between these two disciplines is where the real value is created.

The goal is controlling when and how you pay taxes, not just deferring them. Installments let you fill up moderate brackets year after year instead of pushing a single spike into the top rates.

The Payout Election: Matching the Length to Your Gap

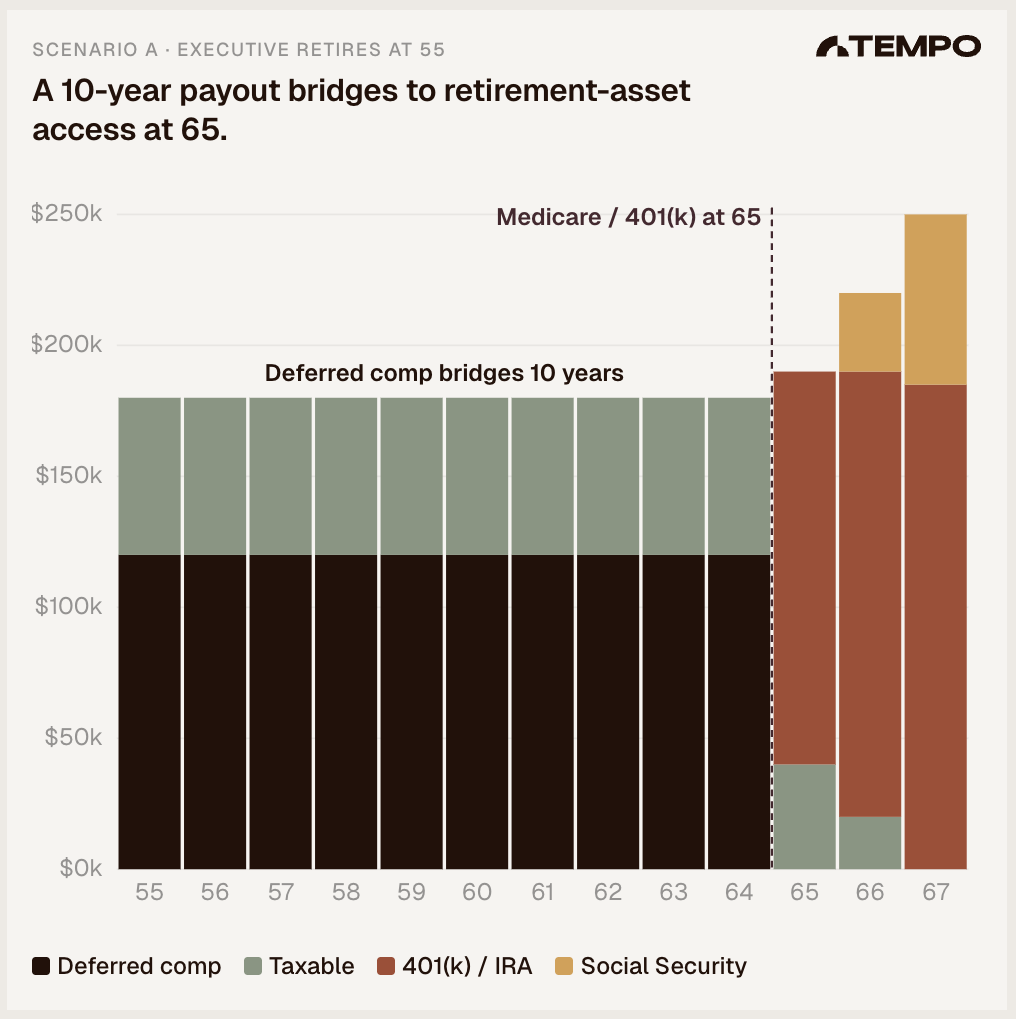

Under IRC Section 409A, executives must elect distribution timing in advance, often years before retirement, and those decisions are difficult to change after the fact. The right payout length isn’t one-size-fits-all. It should be engineered around a specific target: the point at which your other retirement assets become accessible.

Consider two executives. One retires at 55 with a full decade before Medicare eligibility and years before it makes sense to touch their 401(k). A 10-year deferred comp payout makes sense: it bridges the entire gap, manages tax brackets throughout, and allows retirement account assets to continue compounding untouched.

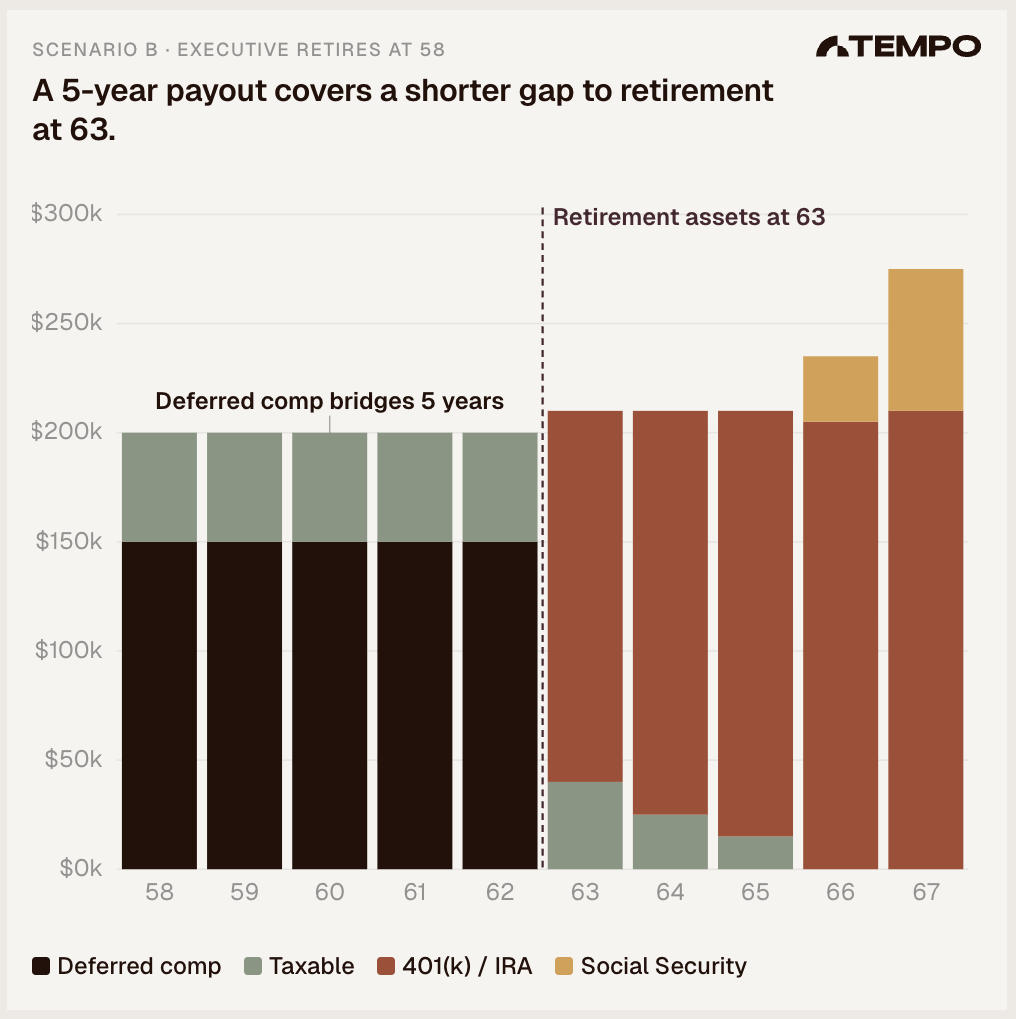

A second executive retiring at 58 has a much shorter runway to reach the same finish line. A 5-year payout covers the gap efficiently without unnecessary exposure to employer credit risk.

Scenario A – Age 55

10-year payout

Longer gap to retirement assets. Deferred comp bridges to age 65 (Medicare eligibility), manages tax brackets throughout, and allows 401(k) assets to compound untouched for a full decade.*

Scenario B – Age 58

5-year payout

Shorter gap to retirement assets. Five years of deferred comp bridges to age 63, when 401(k) and IRA assets are accessible. With less runway needed, a shorter payout suffices.

What these charts make clear is that deferred comp doesn’t exist in isolation. It works in concert with every other asset an executive has accumulated. When a comprehensive income plan is built around the full picture – taxable brokerage accounts, 401(k) and IRA balances, equity compensation, Social Security timing, and deferred comp distributions – each source can be drawn from in the order and amount that keeps the executive in the most favorable tax brackets possible year after year.

The result is more income retained, less surrendered to federal and state tax authorities, and a retirement that runs on the executive’s terms rather than the IRS’s schedule.

The sequencing of these assets is the strategy. Getting it right requires a deliberate, coordinated plan built around each executive’s unique income picture, risk profile, and retirement goals.

*These scenarios are presented for illustrative purposes only and do not represent a specific recommendation for any individual. The order, amount, and tax efficiency of drawing from various assets will differ materially based on each person’s situation — including total asset balances, income sources, filing status, state of residence, healthcare needs, and family circumstances. No two retirement income plans are alike, and the examples above are intended only to demonstrate the general principles at work, not to prescribe a course of action.

How Deferred Compensation Is Treated By State Taxes

Many executives assume that moving from a high-tax state like Ohio to a no-income-tax state like Florida will automatically eliminate state taxes on their deferred compensation. The reality is more nuanced.

Whether a state can tax those distributions after you’ve relocated depends heavily on the payout structure elected. Under federal law, distributions paid over 10 or more years in substantially equal installments are generally taxed in the state where the executive resides at the time of payment – meaning a properly structured 10-year payout to a Florida resident may carry no state income tax at all.

By contrast, a shorter payout of fewer than 10 years may still give the original state, Ohio in this case, a valid claim on a portion of those distributions, even after the executive has left. The tradeoff is a key consideration: longer payouts offer greater state tax efficiency, but may not make sense depending on a given executive’s financial situation.

Deferred Comp as an Early Retirement Bridge

NQDC plans play a unique role for executives stepping away before age 59½. Unlike 401(k)s or IRAs, NQDC distributions are not subject to early withdrawal penalties, making them an ideal bridge income source in the years before traditional retirement accounts become accessible without penalties.

When layered correctly with taxable investments and equity compensation, deferred comp becomes a highly customizable income bridge, one that can support early retirement while maintaining tax efficiency across federal and state levels.

Frequently Asked Questions

Is deferred compensation taxable?

Yes. Nonqualified deferred compensation is taxed as ordinary income when you receive distributions, not when the compensation is earned or deferred. This is what makes timing so important – distributions taken in lower-income years are taxed at lower rates than income earned during peak earning years.

How are NQDC plan distributions taxed when you move states?

It depends on payout length. Under federal law, distributions paid over 10 or more years in substantially equal installments are generally taxed in the state where you reside at the time of payment.

A shorter payout may still be subject to tax in the state where the income was originally earned, even after you have relocated. An executive who retires to Florida after working in Ohio can potentially eliminate state income tax on their entire NQDC balance – but only if the payout structure qualifies under the 10-year threshold.

Are NQDC plan distributions subject to early withdrawal penalties?

No. Unlike 401(k) and IRA distributions, NQDC plan distributions are not subject to early withdrawal penalties for amounts taken before age 59½. This makes NQDC plans a particularly effective bridge income source for executives who retire early – they can draw from their deferred compensation without penalty while leaving tax-advantaged retirement accounts untouched to continue compounding.

Want to talk about your deferred comp options?

At Tempo Wealth, our goal is to bring the same structured, principles-based thinking to your deferred compensation planning. If you’d like us to model your payout options, map the tax impact across distribution scenarios, and build an income bridge strategy around your retirement timeline, reach out for a consultation. Send us a message or call 440-568-3676 to get in touch.

Disclosures

Tempo Wealth, LLC ("Tempo") is a Registered Investment Advisor registered with the Securities and Exchange Commission (SEC). Registration as an investment adviser does not imply a certain level of skill or training, and the content of this communication has not been approved or verified by the United States Securities and Exchange Commission or by any state securities authority.

The information contained in this material is intended to provide general information about Tempo and its services. It is not intended to offer investment advice. Investment advice will only be given after a client engages our services by executing the appropriate investment services agreement. Information regarding investment products and services are provided solely to read about our investment philosophy and our strategies. You should not rely on any information provided on our web site in making investment decisions. Market data, articles and other content in this material are based on generally available information and are believed to be reliable. Tempo does not guarantee the accuracy of the information contained in this material. Tempo will provide all prospective clients with a copy of our current Form ADV, Part 2A (Disclosure Brochure) prior to commencing an advisory relationship. However, at any time, you can view our current Form ADV, Part 2A at adviserinfo.sec.gov. In addition, you can contact us to request a hardcopy.

This article discusses general planning considerations and does not take into account any individual’s specific financial situation. Strategies discussed may not be appropriate for all investors. Examples are provided solely to illustrate a common planning scenario following a large dividend and are not a recommendation to buy, sell, or hold any security, including shares of The Progressive Corporation.