For many executives at publicly traded companies, company stock is often more than compensation. It can be a meaningful piece of your retirement savings inside a 401(k). And when those shares have appreciated significantly over time, the way you distribute them at retirement or a job change can have a major impact on your long-term tax bill. One of the most powerful and underused strategies for handling this is Net Unrealized Appreciation (NUA).

What Is Net Unrealized Appreciation (NUA)?

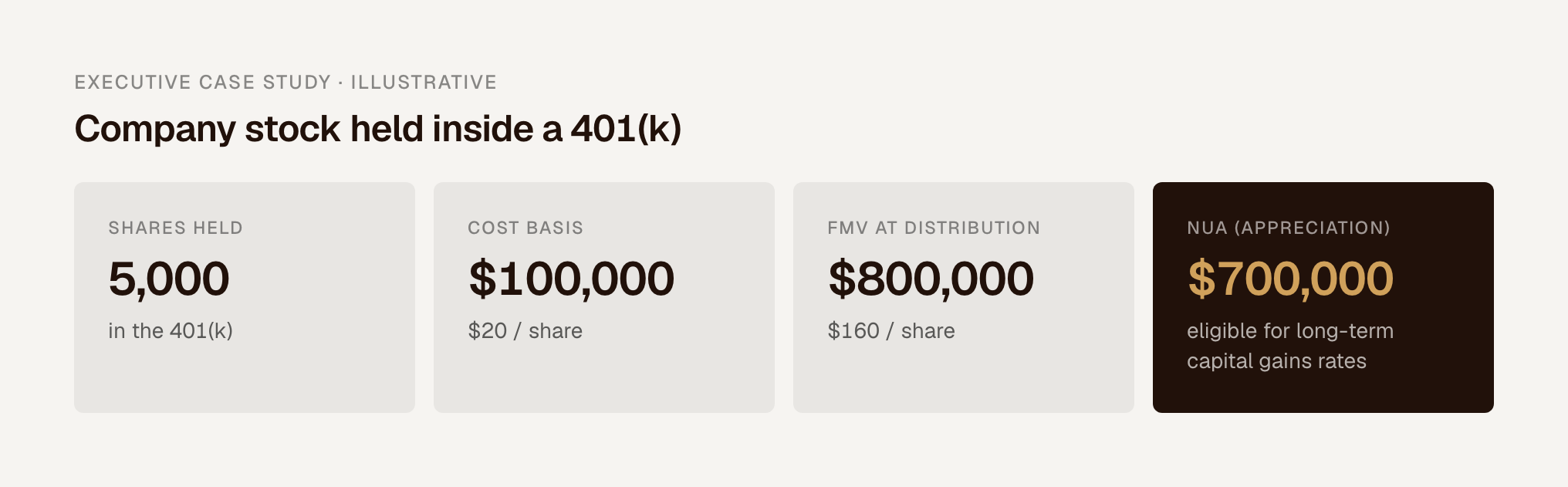

NUA is the difference between the original cost basis of your company stock (what you paid for it inside the plan) and what it's worth when you take a distribution.

Under a standard 401(k) rollover, the entire value, both cost basis and appreciation, eventually gets taxed as ordinary income. With NUA, you take a different path:

- You move your employer stock in-kind to a taxable brokerage account

- You roll the remainder of your 401(k) into an IRA

- You pay ordinary income tax only on the cost basis in the year of distribution

- The appreciation is taxed later at long-term capital gains rates when you sell, which are significantly lower for most executives

Who Qualifies for NUA?

Two conditions must both be met to use this strategy:

1. A qualifying "triggering event" must occur. The IRS recognizes four:

- Separation from service. The most common path for executives who retire, resign, or otherwise leave the employer sponsoring the plan.

- Attaining age 59½. Even if still employed, this age milestone qualifies you for a lump-sum distribution.

- Disability. Total and permanent disability triggers NUA eligibility.

- Death. Beneficiaries may use NUA rules under certain conditions.

A note on the Rule of 55: This rule allows penalty-free withdrawals from your current employer's 401(k) after separation in or after the year you turn 55 — but it does not by itself create an NUA triggering event. It affects penalty treatment only.

2. You must take a lump-sum distribution of your entire 401(k) plan (across all like plans with the same employer) in the same tax year as the triggering event. This means all non-company stock assets — mutual funds, target-date funds, bonds, and any other holdings in the plan — must be rolled over to a traditional IRA in the same transaction.

Failing to do so, or distributing those assets as cash, could disqualify the entire NUA election and trigger ordinary income tax on the full account balance. The in-kind stock transfer and the IRA rollover of remaining assets should be executed together, ideally coordinated in advance with your plan administrator and financial advisor.

NUA in Action: A Tax-Savings Example

Let's look at a concrete example using 5,000 shares of company stock held inside a 401(k). The executive has separated from service at age 60 and takes a lump-sum distribution in the same tax year.

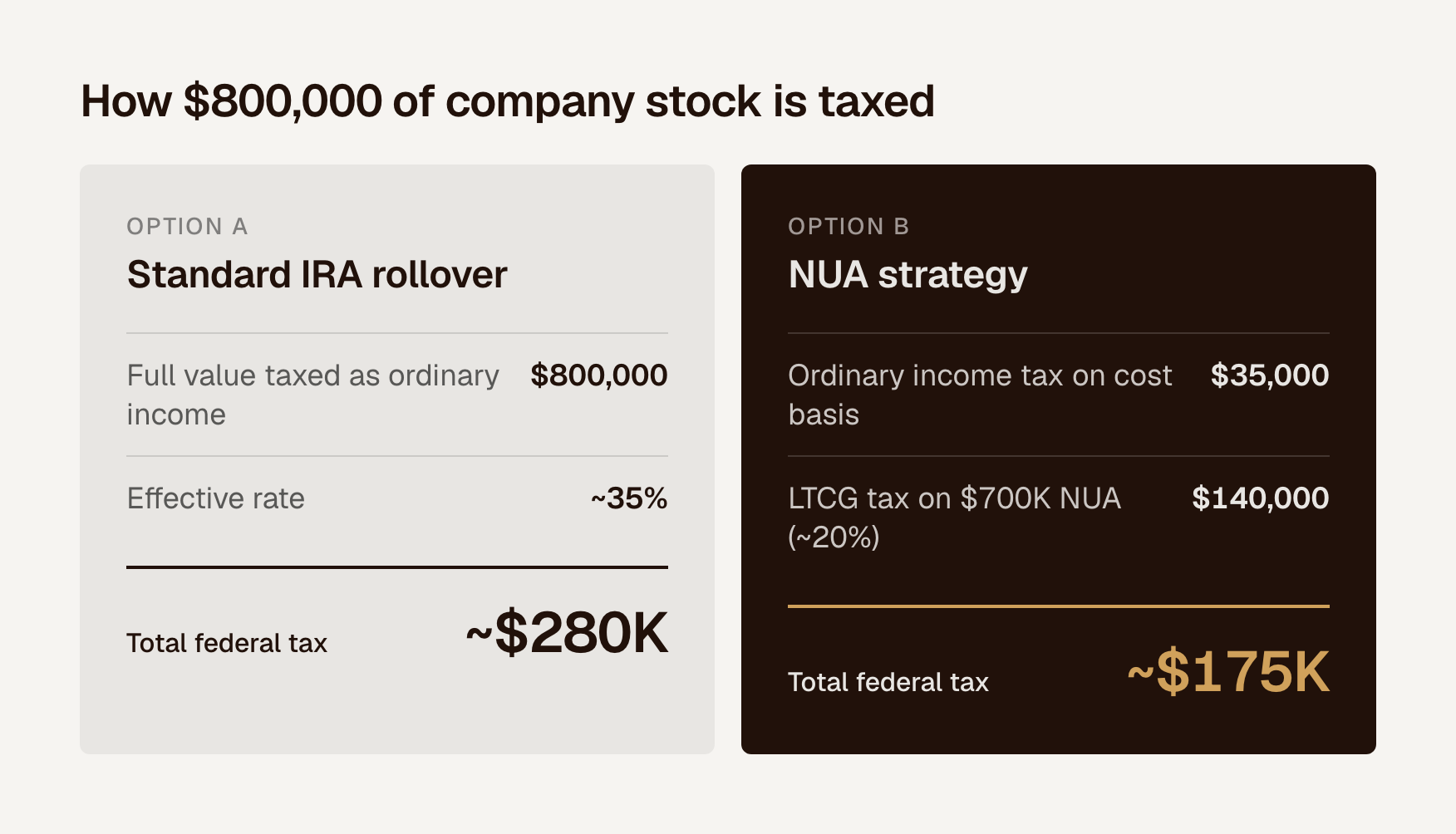

Assuming the executive was in the 35% federal tax bracket at retirement in both situations, here's a general look at the potential tax savings over time:

Tax Burden Comparison

The chart below illustrates how each dollar is taxed under each approach on $800,000 of company stock (estimated at ~35% ordinary income rate and ~20% long-term capital gains rate):

When NUA May Not Make Sense

NUA isn't the right move in every situation. It may not make sense if:

- The stock hasn't appreciated significantly — a low NUA means minimal tax benefit

- Diversification is a higher priority than tax efficiency

- Your plan doesn't permit the required in-kind transfers

The IRS rules around triggering events, lump-sum timing, and cost basis reporting are specific, and the window to act is narrow. This is a strategy that benefits from early, coordinated planning with your financial advisor, CPA, and estate attorney well before retirement or separation.

Let's Build Your Equity Compensation Strategy

At Tempo Wealth, our goal is to be a trusted resource with structured, principles-based planning for maximizing equity compensation — both during "business-as-usual" planning and in surprise moments like variable compensation changes and retirement income planning.

To learn more about how we think about executive compensation management, download our Executive Equity Compensation Guide.

If you'd like us to review your current holdings, model the after-tax impact, and build an equity-comp strategy aligned with your goals, reach out for a consultation. Call 440-568-3676 or email info@tempowealth.com.

Disclosures

Tempo Wealth, LLC ("Tempo") is a Registered Investment Advisor registered with the Securities and Exchange Commission (SEC). Registration as an investment adviser does not imply a certain level of skill or training, and the content of this communication has not been approved or verified by the United States Securities and Exchange Commission or by any state securities authority. The information contained in this material is intended to provide general information about Tempo and its services. It is not intended to offer investment advice. Investment advice will only be given after a client engages our services by executing the appropriate investment services agreement. Information regarding investment products and services are provided solely to read about our investment philosophy and our strategies. You should not rely on any information provided on our web site in making investment decisions.

Market data, articles and other content in this material are based on generally available information and are believed to be reliable. Tempo does not guarantee the accuracy of the information contained in this material. Tempo will provide all prospective clients with a copy of our current Form ADV, Part 2A (Disclosure Brochure) prior to commencing an advisory relationship. However, at any time, you can view our current Form ADV, Part 2A at adviserinfo.sec.gov. In addition, you can contact us to request a hardcopy.

This article discusses general planning considerations and does not take into account any individual's specific financial situation. Strategies discussed may not be appropriate for all investors. Examples are provided solely to illustrate a common planning scenario for individuals where NUA could be an option.