Most executives at public companies have solid benefit packages on paper: group life insurance, supplemental life, long-term disability, health coverage, deferred compensation, and equity awards. But are those benefits sized correctly for your income, your household, and the risks you actually carry?

Below, we’ll explore different benefit areas that deserve a closer look and how to think about them.

Life Insurance: Coverage Tied to Employment Is Coverage You Do Not Control

Group life insurance is typically a multiple of base salary. That formula ignores bonuses, RSUs, deferred compensation balances, mortgage payoffs, college funding, and a surviving spouse's long-term income needs. It also disappears, or changes significantly, when you retire, change companies, or leave on someone else's terms.

There is also a tax consideration worth knowing. Employer-provided group-term life insurance above $50,000 generates taxable imputed income under IRS rules. For executives carrying substantial employer-provided coverage, that cost is real and worth factoring into the overall picture.

Supplemental group life deserves a separate look. Many executives default to it because it is convenient, but group premiums typically step up in five-year age bands and reflect the health experience of the entire employee population, not yours individually. If you are healthier than average, individual term coverage may be more cost-effective over a 20- or 30-year period, and unlike group coverage, it is portable.

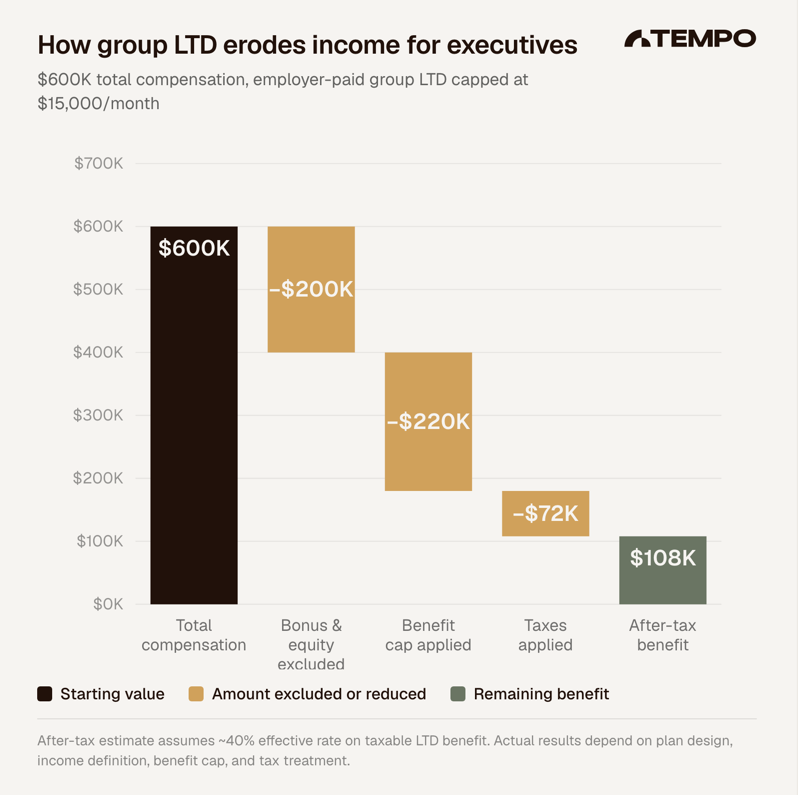

Disability: Why Group Long-Term Disability Falls Short for Executives

Group long-term disability plans are often designed around base salary only, and most carry a monthly benefit cap. For executives whose total compensation includes annual bonuses, RSUs, stock options, performance shares, or deferred compensation distributions, the effective replacement ratio can be far lower than the stated 60%.

Tax treatment amplifies the gap. When the employer pays disability premiums, benefits are generally taxable. A plan that replaces 60% of base salary on a pre-tax basis may deliver considerably less after-tax income than expected during a disability.

Consider the following example:

Reviewing the definition of covered earnings, the benefit cap, elimination period, tax treatment, and whether individual supplemental disability coverage closes the gap is a core part of executive financial planning.

Property, Liability, and Umbrella Coverages: The Exposures Executives Tend to Underestimate

Risk management does not stop at life and disability. Higher-net-worth households should review homeowners coverage, auto liability limits, umbrella liability, scheduled valuables, cyber protection, and identity theft resources on a regular basis.

Executives often carry exposure that a standard homeowners or auto policy was not designed to cover, such as teenage drivers, rental properties, vacation homes, household employees, pools, public visibility, charitable board roles, or outside director positions. A personal umbrella policy extends liability protection above the underlying home and auto limits, typically after those base limits are exhausted.

There is no fixed formula for how much umbrella coverage you need, but comparing existing liability limits against net worth and future earning capacity is a useful starting point. An executive household with $3 million in net worth and $500,000 in underlying liability coverage has a significant gap if a serious claim occurs.

Executives serving on outside boards should also understand what directors and officers coverage applies, and where it stops, for each organization.

The Integration Question

Executive benefits are a starting point, not a complete plan. A coordinated planning process connects employer benefits, personal insurance, property and casualty coverage, estate documents, and investment risk into a single picture. The goal is to make sure that years of building wealth through compensation, equity, and disciplined saving are not disrupted by one event that the right coverage would have addressed.

Before assuming your benefits are sufficient, review them alongside your full compensation picture, family needs, and financial plan.

Disclosures

This article is for informational purposes only and does not constitute financial, legal, or insurance advice. Coverage needs vary by individual circumstances. Please consult a qualified financial advisor and licensed insurance professional before making decisions about your coverage. Tempo Wealth Management is a registered investment adviser.

Tempo Wealth, LLC ("Tempo") is a Registered Investment Advisor registered with the Securities and Exchange Commission (SEC). Registration as an investment adviser does not imply a certain level of skill or training, and the content of this communication has not been approved or verified by the United States Securities and Exchange Commission or by any state securities authority.

The information contained in this material is intended to provide general information about Tempo and its services. It is not intended to offer investment advice. Investment advice will only be given after a client engages our services by executing the appropriate investment services agreement. Information regarding investment products and services are provided solely to read about our investment philosophy and our strategies. You should not rely on any information provided on our web site in making investment decisions. Market data, articles and other content in this material are based on generally available information and are believed to be reliable. Tempo does not guarantee the accuracy of the information contained in this material. Tempo will provide all prospective clients with a copy of our current Form ADV, Part 2A (Disclosure Brochure) prior to commencing an advisory relationship. However, at any time, you can view our current Form ADV, Part 2A at adviserinfo.sec.gov. In addition, you can contact us to request a hardcopy.